Got an ASMT-10 Notice? Here's What It Means — And Why How You Reply Decides Everything

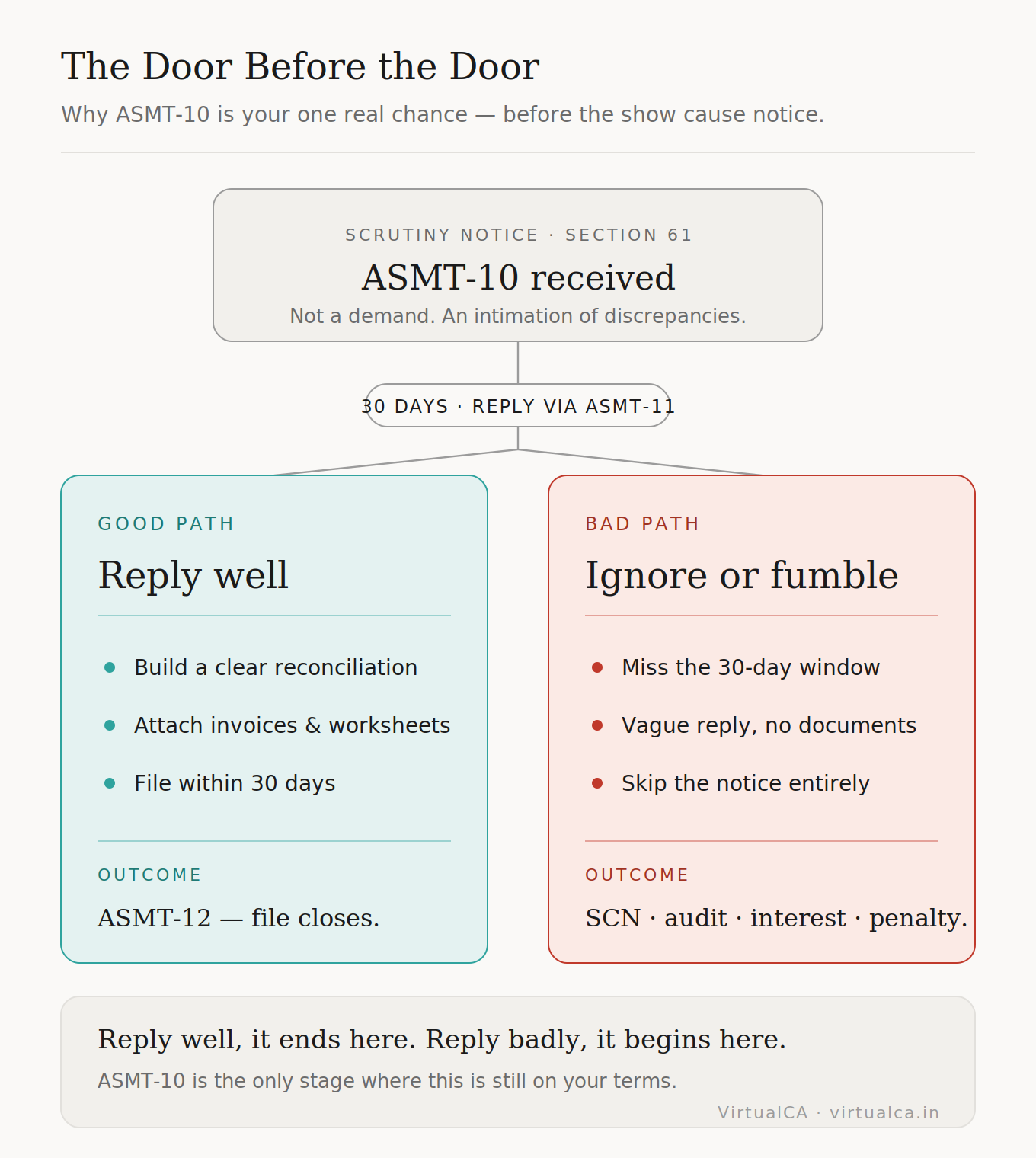

If you've just received an ASMT-10 notice on the GST portal, the first instinct is usually to panic. Don't. An ASMT-10 isn't a demand. It isn't a penalty. It's something more important to understand correctly — a scrutiny notice from the GST department telling you they've spotted discrepancies in your filed returns and would like an explanation.

Think of it as the door before the door. Reply well, and the matter closes quietly. Ignore it, or reply badly, and the next notice you see is the show cause notice — and from there, the conversation becomes far more expensive.

Here's everything an Indian business needs to understand about ASMT-10, from the legal basis to the practical reply, in plain language.

The legal basis: Section 61 + Rule 99

ASMT-10 is issued by the proper officer under Section 61 of the CGST Act, 2017, read with Rule 99 of the CGST Rules. The provision authorises the officer to scrutinize a registered person's return and related particulars, identify discrepancies, and call for an explanation before taking any further action.

Crucially, ASMT-10 is not a demand notice. It's an intimation of discrepancies, and the entire idea behind Section 61 is to give the taxpayer an opportunity to rectify or explain before any escalation.

Why this stage matters more than people realise

This is the part most businesses miss. ASMT-10 is the pre-SCN stage — the GST department's way of saying, here's what we're seeing; convince us it's fine, or pay up. If you provide a satisfactory reply, the officer issues a closure order in Form ASMT-12 and the file shuts. If you don't, the next step isn't another friendly nudge — it's an audit under Section 65, inspection under Section 67, or a full show cause notice and demand under Section 73 (non-fraud) or Section 74 (fraud/suppression), each carrying interest at 18% and penalties ranging from 10% to as much as 100% of the tax involved.

There's also a strong procedural protection here that's worth knowing. Courts have held that issuance of ASMT-10 is mandatory before initiating proceedings under Section 73 — and where the department skips this step, the subsequent demand can be challenged as procedurally invalid. The point being: this stage isn't optional paperwork. It's a real legal opportunity, and how you use it shapes everything that follows.

What triggers an ASMT-10?

The GSTN's analytics engine quietly cross-references every return you file against the rest of the data it holds. The most common triggers we see in practice are:

- GSTR-1 vs GSTR-3B mismatch — outward supplies declared in GSTR-1 don't match the tax paid in GSTR-3B.

- GSTR-3B vs GSTR-2B mismatch — ITC claimed in GSTR-3B exceeds the eligible credit auto-populated in GSTR-2B.

- E-way bill vs GSTR-1 mismatch — e-way bills generated suggest higher turnover than declared in returns, hinting at unreported sales.

- Ineligible ITC under Section 17(5) — credit claimed on blocked items like food and beverages, club memberships, or personal-use vehicles.

- Missing ITC reversals under Rule 42/43 — common where exempt and taxable supplies coexist.

- Purchases from cancelled or suspended dealers — ITC claimed against a supplier whose GSTIN was retroactively cancelled.

- Annual return mismatches — GSTR-9 totals not matching the sum of monthly returns.

- External data mismatches — turnover declared in returns doesn't tie up with TDS/TCS data, income-tax filings, or bank credits.

Each of these has a perfectly defensible explanation in many cases — but only if you actually respond, with documents.

The 30-day window

Once ASMT-10 is served, you have 30 days from the date of service to file your reply in Form ASMT-11, with the option to seek an extension from the officer if needed. Miss this window, and the officer can proceed to the next stage without further intimation.

A few procedural points worth knowing:

- Notices are served electronically — they appear under View Additional Notices and Orders on the GST portal. Many businesses miss them simply because they don't check this section.

- The officer is generally expected to quantify the discrepancy and attach worksheets while issuing ASMT-10. If the notice is vague or unsupported, that itself can be a defence ground.

- An ASMT-10 can't be issued repeatedly for the same grounds in the same financial year — though new grounds for the same year can attract a fresh notice.

Three ways your reply can go

Every ASMT-11 reply falls into one of three buckets:

1. You agree fully with the officer. Pay the differential tax along with interest through DRC-03, then file ASMT-11 referencing the payment with all challan details. This is the cleanest closure.

2. You partly agree. Pay what you accept via DRC-03, and contest the rest in ASMT-11 with reasoning and documents.

3. You disagree entirely. File ASMT-11 with a clear, evidence-backed explanation. No payment is required in this case; the strength of your reply is what decides the outcome.

What a strong ASMT-11 reply looks like

A reconciliation statement is the backbone of every good reply. For each discrepancy the officer has flagged, your reply should show — line by line, invoice by invoice where needed — exactly why the numbers look the way they do.

A few practical pointers:

- Build the reconciliation party-wise and invoice-wise. Especially for GSTR-2A/2B vs GSTR-3B mismatches, identify which supplier delayed filing GSTR-1, in which month their invoice eventually surfaced in your 2B, and that you claimed ITC only when it became eligible.

- For FY 2017-18 and FY 2018-19 ITC issues, refer to CBIC Circular No. 183/15/2022-GST dated 27 December 2022, which lays out the procedure for situations where suppliers failed to report invoices.

- Attach supporting documents — invoices, e-way bills, payment proofs, bank statements, vendor confirmations, and the reconciliation worksheets themselves.

- Address each point the officer raised, in the same order. A reply that wanders, or only addresses some of the discrepancies, invites further scrutiny.

- Keep the ARN of your ASMT-11 reply safe and track the status on the portal.

Mistakes that turn an ASMT-10 into a much bigger problem

We see the same avoidable errors repeatedly: rushing the reply without proper reconciliation, ignoring the notice in the hope it goes away, treating it as an informal query, or accepting the officer's number without checking whether the underlying data is even correct. Any of these can convert a routine scrutiny into a Section 73 demand with penalty and interest, or push the case into a full audit. The cost of doing the reply properly is almost always a fraction of the cost of doing it badly.

The bottom line

ASMT-10 is the GST department telling you, in writing, exactly where they think your returns don't add up — and giving you a structured window to explain. Treated seriously, it closes with an ASMT-12 and a clean compliance record. Treated casually, it becomes an SCN, a demand, an audit, and a fight you didn't need to have.

At VirtualCA, we handle ASMT-10 notices end-to-end for startups and growing SMEs — reading the notice properly, building the GSTR-1/3B/2B/e-way-bill reconciliations, drafting the ASMT-11 reply with the right legal references, and tracking it through to closure. If you've just received one, don't sit on it — the 30-day clock is already running.

Comments