Your Employer May Soon Deduct SIPs Directly From Your Salary — What SEBI's New Proposal Actually Means

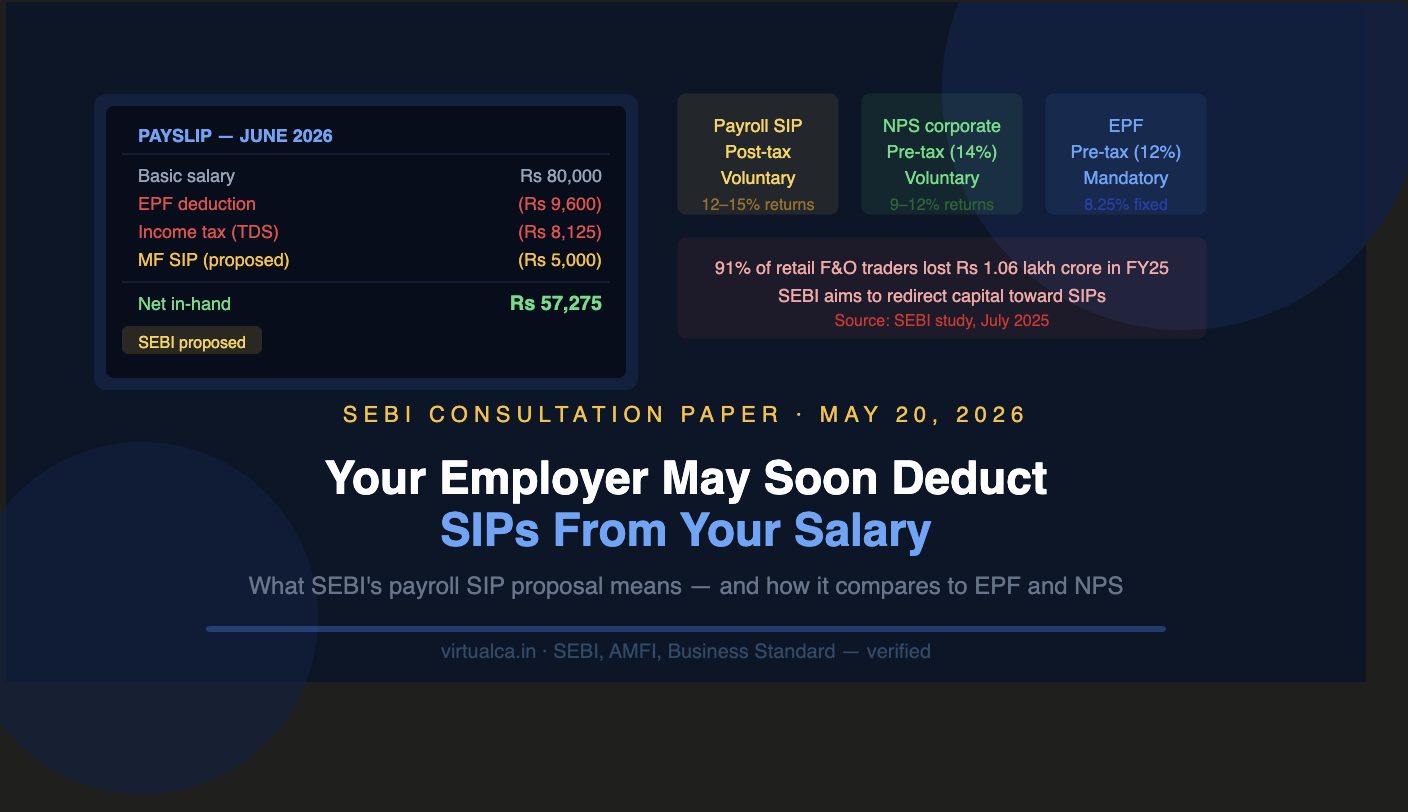

Imagine opening your June salary slip and seeing a new line item: "Mutual Fund SIP — Rs 5,000." Just like your EPF contribution, it's already been invested on your behalf before the money even hit your account.

That's exactly what SEBI is proposing. On 20 May 2026, SEBI released a draft consultation paper proposing a significant change in mutual fund investment rules — enabling companies to deduct money directly from employees' salaries for mutual fund investments under a third-party payment framework. Public comments on the proposal were invited until 10 June 2026. Here's a clear breakdown of what's being proposed, why SEBI is doing it, how it compares to EPF and NPS, and what it actually means for your wallet.

Why is SEBI proposing this now?

Two hard numbers are driving this proposal.

First, the F&O crisis. Individual traders' net losses in the equity derivatives segment rose to Rs 1,05,603 crore in FY25, up 41% from Rs 74,812 crore in FY24. Over 91% of individual traders made losses in the equity derivatives segment. Young traders under 30 made up 43% of this loss-making cohort — many of them earning less than Rs 5 lakh annually. By creating a friction-free payroll route for SIPs, SEBI hopes to redirect volatile speculative capital toward long-term, professionally managed mutual funds.

Second, the FII dependency problem. By the first week of May 2026, Foreign Portfolio Investors had pulled Rs 1.92 lakh crore out of Indian equities, already eclipsing the entire 2025 sell-off in just four months. The primary stabilising force has been domestic SIP investors. SIP contributions stayed around Rs 30,000 crore through the volatility, reaching Rs 31,115 crore in April 2026, up 16.8% year-on-year. DIIs more than fully absorbed FII selling in the most volatile months. A broader, deeper domestic SIP base is SEBI's long-term answer to foreign capital volatility.

How would payroll SIPs actually work?

The mechanism mirrors EPF. Your employer deducts a fixed amount from your gross salary each month and routes it directly to an Asset Management Company (AMC) of your choice. The key differences from EPF are that participation is entirely voluntary for both employer and employee, and you can choose any mutual fund scheme — equity, debt, hybrid, or gold.

Under the proposal, mandatory KYC verification, relationship checks between investor and payer, transaction tracking, and ensuring that redemption and dividend proceeds continue to be credited only to verified investor bank accounts would be retained as anti-money laundering safeguards. Your employer can never touch the redemption proceeds — when you sell, the money goes directly to your personal bank account, not back to the company.

The facility would be available to employees of all listed companies and EPFO-registered firms. Participation remains voluntary for employees, and SEBI said the proposed framework seeks to strike a balance between ease of investing and regulatory protection.

How does it compare to EPF and NPS? The key differences that matter

This is where most coverage gets it wrong. People assume payroll SIPs are equivalent to EPF or NPS. They aren't — and the differences have real financial consequences.

| Feature | Payroll SIP (proposed) | NPS (corporate) | EPF |

| Nature | Voluntary | Voluntary | Mandatory |

| Tax treatment | Post-tax investment | Pre-tax (up to 14% of basic) | Pre-tax (12% of basic) |

| Returns (historical) | 12–15% (equity, market-linked) | 9–12% (market-linked) | 8.25% fixed (FY25) |

| Tax at withdrawal | LTCG/STCG applicable | 60% lump sum tax-free; 40% annuity | 100% tax-free (EEE) |

| Liquidity | High — no mandatory lock-in | Locked till age 60 | Locked till retirement |

| 30-year corpus (Rs 10K/month gross) | Rs 2.43 crore (after tax) | Rs 2.09 crore + pension | Rs 1.58 crore (fully tax-free) |

The single most important distinction is the pre-tax vs post-tax difference. When your employer contributes to NPS under Section 124(2), that money is deducted from your gross salary before your income tax is calculated. Your taxable income falls. For a 30% tax bracket employee, every Rs 1,000 invested in employer NPS costs you only about Rs 688 in take-home pay — because the Rs 312 that would have gone to the government as tax is instead going into your NPS account. A payroll SIP, by contrast, is made from post-tax income — the full Rs 1,000 reduction hits your take-home, with no tax benefit.

In practical terms, this means that for the same reduction in monthly take-home pay, the pre-tax NPS route puts roughly 45% more capital into active compounding from day one than a payroll SIP. Over 30 years, this gap compounds significantly.

The tax picture is simple: payroll SIPs offer no new tax break

If you invest in a payroll SIP in a regular equity mutual fund, there is no deduction from your taxable income under the new tax regime. The only way to get a tax benefit via a payroll SIP is by choosing an ELSS (Equity Linked Savings Scheme) — but that deduction is capped within the Rs 1.5 lakh Section 80C limit, which is not available at all under the new default tax regime.

For most salaried employees filing under the new regime, a payroll SIP is simply a convenience mechanism — not a tax-saving tool. It automates investment discipline but does not reduce your tax bill.

The real benefits and the real risks

The genuine upside of payroll SIPs is behavioural. Many people intend to invest but miss SIP dates, run short on account balances, or redirect the money elsewhere before month-end. Payroll deduction enforces the "save first, spend later" principle — the same reason EPF works so well as a retirement corpus builder. For first-time investors or those with weak investment discipline, this automation could genuinely build wealth over time.

The risks are equally real. If your employer partners with specific AMCs for operational convenience, you may face subtle institutional pressure to choose those funds over better alternatives. NAV timing is also a concern — payroll SIPs involve bulk employer transfers, which can get delayed past daily cut-off times, meaning you could receive a less favourable purchase price than a direct bank-to-AMC SIP investor. And corporate HR teams will need to manage voluntary, individually-customised deductions for hundreds of employees — a significant operational overhead that many employers may simply choose to skip.

What should you actually do?

For salaried employees who already have automated bank mandates for SIPs, the honest answer is that the payroll route adds convenience but not financial superiority. Your direct SIP already enforces discipline, gives you full control over AMC selection, and avoids any employer-linked conflict of interest.

Where payroll SIPs could make a meaningful difference is for employees who genuinely struggle with SIP consistency — particularly those in the early stages of their careers who have never set up a mandate. For this group, an automated payroll deduction could be the nudge that starts a 30-year compounding journey.

For higher-income employees in the 30% bracket, the pre-tax compounding advantage of maximising employer NPS (up to 14% of basic) first is far superior to a post-tax mutual fund payroll SIP. Use the payroll SIP route for discretionary equity investing after the NPS slot is fully utilised.

SEBI's proposal is not yet finalised. Watch this space — if implemented, it will reshape how salaried India approaches long-term wealth building.

Need help structuring your salary for maximum after-tax investment efficiency? Reach out to Virtualca Services.

Comments