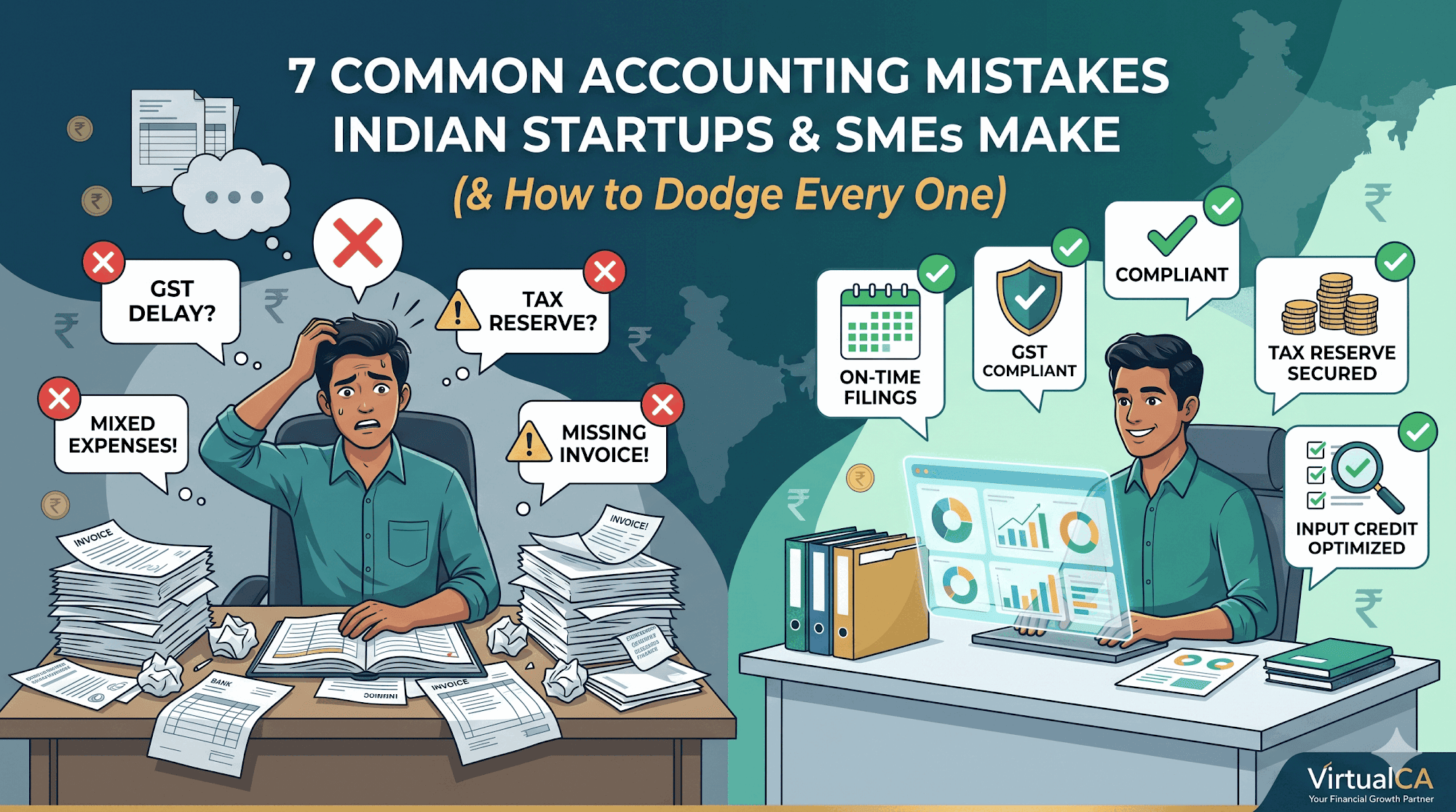

7 Accounting Mistakes Indian Startups & SME Businesses Make (And How to Dodge Every One)

Starting a business is exciting. You're chasing your first clients, building the thing you've dreamed about, finally watching money move in your direction. But here's the quiet truth nobody puts on the launch-day highlight reel: getting your accounts wrong can cost you far more than you'd expect — in penalties, in lost input credits, and in sleepless nights before every due date.

The good news? Almost every early-stage accounting disaster comes down to one of seven mistakes. And every single one is avoidable.

1. Mixing business and personal money

It's the most common slip-up of all. When cash is tight, swiping your personal account feels harmless — but it turns expense tracking into a nightmare and weakens your position if the books are ever questioned. Open a dedicated business current account on day one, before the first invoice, before the first sale.

2. Putting off bookkeeping

Plenty of founders pile up bills and bank statements and promise to "sort it at year-end." By then, it's chaos — and chaos is expensive to untangle. Set up simple bookkeeping from the start. Tools like Tally, Zoho Books, or QuickBooks make it almost painless and grow with you as you scale.

3. Missing the GST registration threshold

This one bites hard. Once your aggregate turnover crosses ₹40 lakh for goods (or ₹20 lakh for services) — and lower limits of ₹20 lakh / ₹10 lakh in special-category states — GST registration isn't optional. Cross it unnoticed and you can be liable for tax from the date registration became due, plus interest and penalty, with input credit blocked for the gap. Watch your rolling turnover every month and register on time.

4. Poor record keeping

A lost invoice isn't just untidy — it's a missed ITC claim or a disallowed expense waiting to happen. Go digital. Snap photos of bills the moment you receive them, store everything in the cloud, and keep your purchase invoices matched against your GSTR-2B. Your future self (and your auditor) will thank you.

5. Not setting aside money for tax

Surprise tax outflows catch startups off guard more than almost anything else. Spend every rupee you earn today, and advance tax instalments in June, September, December and March become a recurring panic. A solid rule of thumb: park at least 25–30% of your profits aside for tax, somewhere you won't be tempted to touch.

6. Trying to do it all alone

Handling your own compliance feels like a smart way to save money. Often, it's the opposite — the penalties you trigger and the reliefs you miss can dwarf any fee you avoided. Engage a CA early. Even ongoing part-time support can save you many times its cost and free you to actually run the business.

7. Missing deadlines

Late GST returns, delayed TDS payments, and missed ROC or income-tax filings come with automatic penalties, interest, and a lot of avoidable stress. Map out every recurring due date — GSTR-1, GSTR-3B, TDS returns, advance tax, ROC annual filings, and your ITR — mark them in your calendar, and set reminders well ahead.

The bottom line

None of these mistakes happen because founders are careless. They happen because building a business is all-consuming, and compliance quietly slides to the bottom of the pile. The founders who get this right aren't accounting experts — they just build a few simple habits early: a separate account, clean digital records, money set aside, and someone in their corner who knows the rules.

Get those basics in place, and your accounts stop being a source of dread and become what they should be — a clear view of a business that's working.

At VirtualCA, that's exactly what we help startups and growing SMEs do. If your books feel like a weight rather than a window, don't wait for year-end — a little help early goes a long way.

Comments