A Bookkeeper's Week and Month: What It Really Looks Like for an Indian SME

Most founders know they need their books kept, but few picture what the work actually involves. In India, there's an added layer that businesses elsewhere don't face quite so intensely: bookkeeping isn't just about tidy records — it directly feeds a monthly GST and TDS compliance calendar with hard deadlines and real penalties. Fall behind on the books, and you fall behind on filings.

So the work settles into a rhythm — a few tasks that repeat every week, and bigger ones that come around every month. Here's what that rhythm looks like for a typical Indian startup or SME.

One caveat first: every business is different. A small trader under the QRMP scheme (turnover up to ₹5 crore) files GST quarterly; a larger one files monthly. Not every task below applies to everyone — but together they paint an accurate picture.

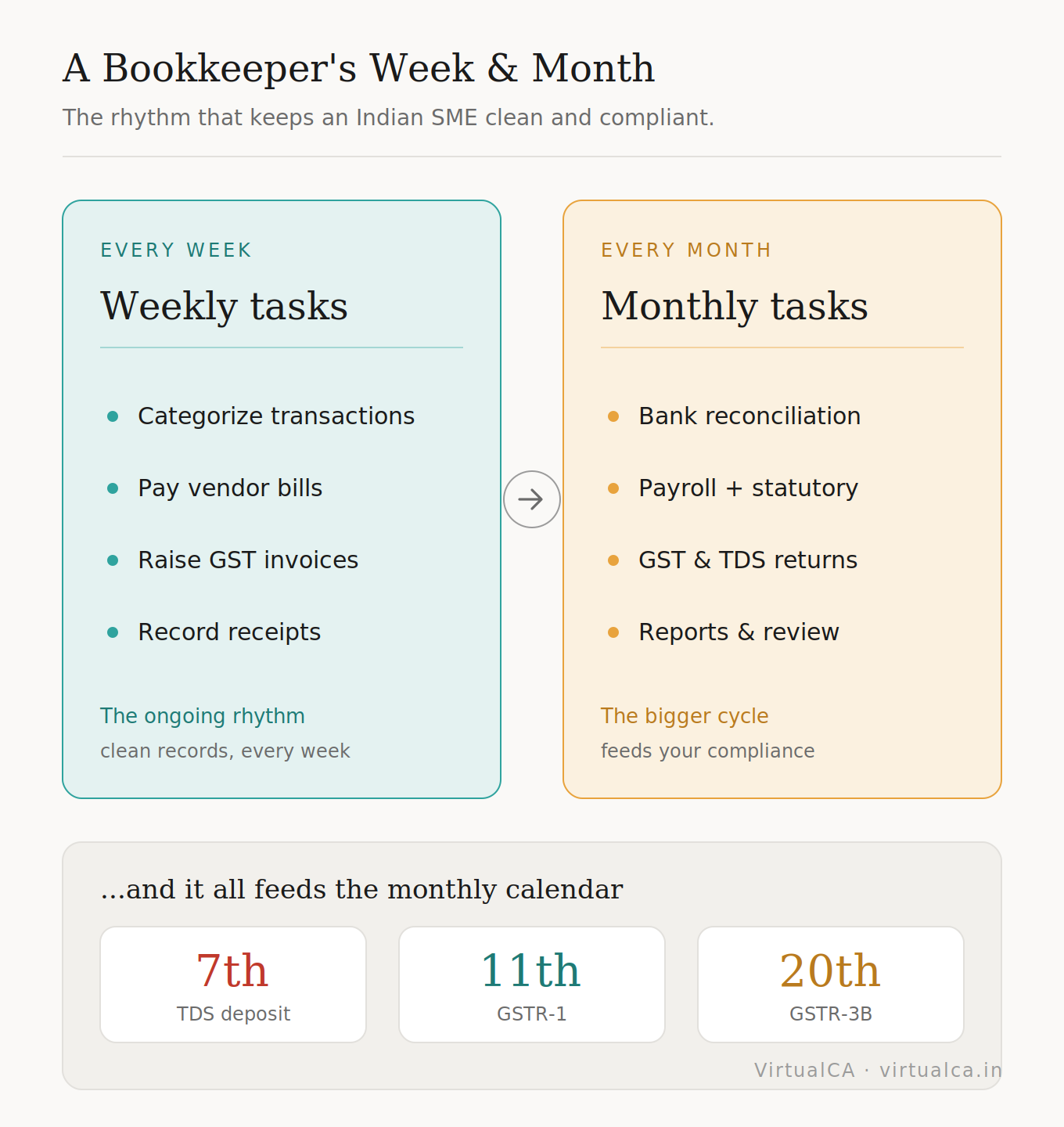

The weekly tasks

1. Categorizing transactions. This is the bread and butter. Every payment and receipt gets sorted into the right ledger head, with the correct GST treatment and input-tax-credit eligibility flagged. Done weekly in Tally, Zoho Books, Vyapar, or QuickBooks, it keeps month-end from becoming a nightmare — and it's the foundation everything else is built on.

2. Paying bills. Vendor bills arrive on all sorts of dates. They rarely need same-day payment, but clearing them on a weekly or fortnightly basis keeps suppliers happy, protects your credit terms, and ensures purchase invoices are captured for ITC.

3. Raising invoices. This means billing customers for what they owe — as proper GST-compliant tax invoices carrying your GSTIN and the right HSN/SAC codes (and e-invoicing where your turnover requires it). Picture a contractor who finished five jobs this week: someone has to raise those five invoices correctly so the money — and the GST trail — starts flowing.

4. Recording receipts. When a customer pays, the matching invoice is marked settled, so the books always reflect what's actually been collected versus what's still outstanding. These four tasks tick along continuously through the month.

The monthly tasks

1. Bank reconciliation. Once a month, the books are matched against the bank statement so every entry lines up. Most tools now pull bank feeds automatically, which makes this far smoother — but the monthly check still matters.

2. Payroll — with statutory deductions. Indian payroll isn't just salary. It carries EPF, ESI, professional tax, and TDS on salary, each with its own deposit deadline. Payroll dates are fixed and non-negotiable; staff expect to be paid consistently, on time.

3. GST and TDS compliance. This is the heart of the Indian monthly cycle. The bookkeeping feeds directly into preparing GSTR-1 and GSTR-3B, reconciling purchases against GSTR-2B before claiming ITC, and ensuring TDS is deducted and deposited. The clean books from weeks one to four are what make these filings possible.

4. Sending reports. A profit & loss statement and balance sheet are the standard pair, often alongside an outstanding-receivables list or a GST summary. These turn raw records into something the owner can actually decide with.

5. The client review. Frequency is agreed up front — monthly, quarterly, or as needed — and is the moment to talk through the numbers rather than just file them.

The Indian month, mapped to real deadlines

Here's a practical way to spread the load — and note how it's pinned to actual due dates:

- Days 1–7 (close + TDS): Finish off the previous month's categorizing, pull the bank statement, reconcile, and investigate mismatches. Crucially, TDS deducted during a month must be deposited by the 7th of the following month.

- Days 8–11 (GSTR-1): Finalize outward supplies and file GSTR-1, which for monthly filers is due on the 11th of the following month.

- Days 12–20 (GSTR-3B + reports): Reconcile ITC against GSTR-2B, then file GSTR-3B, where you pay the actual liability — due on the 20th of every month for monthly filers (the 22nd/24th for QRMP filers, depending on the state). Send the monthly reports to the client around now.

- Days 21–end (bills, collections, payroll): Clear pending bills, chase unpaid invoices, collect receipts, and run payroll near month-end, deducting and scheduling EPF, ESI, PT, and salary TDS.

Spreading tasks like this is the whole trick — it stops the 7th–20th compliance window from turning into a recurring panic, especially when you're handling several entities.

What usually sits with the CA, not the bookkeeper

It helps to know what bookkeeping typically doesn't cover. Adjusting entries, trial-balance finalization, and statutory closing are usually handled by the accountant or CA. So is the heavier tax work — advance-tax estimation (payable in June, September, December, and March), the income-tax return, ROC annual filings for companies, and year-end statements like Form 16 and 16A. The bookkeeper's job is to hand all of this over as clean, reconciled data — without which none of it works.

A quick note on jargon, too: "review aged receivables" simply means chasing the invoices your customers still owe. Don't let the terminology intimidate you; the work underneath is refreshingly practical.

The bottom line

In India, good bookkeeping isn't a year-end event — it's a disciplined weekly and monthly rhythm that keeps your records clean and keeps you on the right side of the GST and TDS calendar. Done well, it quietly prevents the penalties, interest, and blocked input credit that catch so many businesses off guard.

At VirtualCA, that's exactly the cadence we run for startups and growing SMEs — categorizing, reconciling, and filing on a reliable schedule — so your books are always ready and your compliance is never a scramble. If your accounts only get attention near a deadline, that's usually the sign it's time to bring in steady support.

Comments