Freelancers: Why Skipping Your ITR Filing Is the Most Expensive Mistake You Can Make

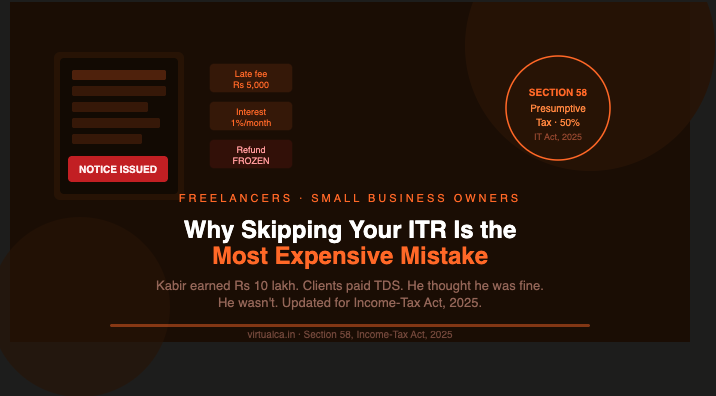

Kabir is a freelance graphic designer. Last financial year was his best yet — Rs 10 lakh in client payments, and his clients had already deducted 10% as TDS. So Kabir did what thousands of freelancers do every year: he assumed the tax was handled, skipped filing his Income Tax Return, and moved on.

Six months later, a notice from the Income Tax Department arrived. What Kabir thought was a minor omission had quietly turned into a financial disaster — penalties, frozen refunds, interest charges, and a rejected home loan application. All because he didn't file a form.

Here's exactly what happened to Kabir — and what every freelancer and small business owner needs to know under the Income-Tax Act, 2025.

Mistake 1: The late fee trap — Section 428

Kabir's first shock was a mandatory penalty just for not filing on time. Under Section 428 of the Income-Tax Act, 2025, failing to furnish your return by the due date attracts a flat fee — Rs 1,000 if your total income does not exceed Rs 5 lakh, and Rs 5,000 in any other case.

Kabir earned Rs 10 lakh. That's a straight Rs 5,000 penalty — regardless of whether he owed any tax at all.

The rule that tripped him: for individuals with business income who are not subject to tax audit, the ITR filing due date for FY 2025-26 is 31 August 2026 — not the 31 July 2026 deadline that applies to salaried individuals. Kabir didn't know he had a different deadline, let alone that crossing it had a fixed monetary cost.

Mistake 2: The hidden interest clock — Section 423

Beyond the flat fee, Kabir owed interest. Under Section 423 of the Income-Tax Act, 2025, any assessee who files after the due date — or does not file at all — is liable to pay simple interest at 1% per month on the amount of unpaid tax, calculated from the day after the due date.

What made this worse: when the Assessing Officer reviewed Kabir's case, certain unexplained expenditures surfaced that Kabir had never documented. His tax liability increased — and the Section 423 interest had been accumulating on the entire enhanced amount throughout the notice period.

Advance tax applies to freelancers whose estimated tax liability for the year exceeds Rs 10,000. It is payable in four quarterly instalments: 15% by 15 June, 45% by 15 September, 75% by 15 December, and 100% by 15 March. Since Kabir had paid no advance tax at all during the year, he faced additional interest on each missed instalment — charges that compounded on top of the Section 423 late-filing interest.

Mistake 3: The frozen refund — Section 431

This is the part that hurt Kabir the most. His clients had deducted Rs 1,00,000 in TDS across the year. After accounting for his legitimate business costs — software subscriptions, internet connection, home office expenses — Kabir's actual tax liability should have been only Rs 40,000. He was entitled to a refund of Rs 60,000.

That money was sitting with the government, waiting for him. But under Section 431 of the Income-Tax Act, 2025, no refund is payable unless a valid return has been filed. By not filing, Kabir effectively gifted Rs 60,000 to the government. Until he files and validates his income and deductions, that refund stays frozen.

This is one of the most common and costly myths among freelancers: that TDS deducted by clients means "tax is done." It is not. TDS is advance tax — money that belongs to you if your actual liability is lower. You can only recover it by filing.

Mistake 4: Mandatory filing even with zero tax owed — Section 263

Kabir made the fundamental error of thinking tax liability and filing obligation are the same thing. They are not. The Income-Tax Act, 2025 mandates filing under Section 263 in several situations regardless of profit or loss:

Under Section 263(1)(a)(ix), any resident who holds a beneficial interest in an asset located outside India — including foreign stocks, foreign bank accounts, or signing authority on overseas accounts — must file a return regardless of income or loss. Kabir had purchased Rs 10,000 worth of US tech stocks. That alone made him legally required to file.

Under Rule 184, you must also file if you spent more than Rs 2 lakh on foreign travel during the year, or if your electricity consumption exceeded Rs 1 lakh. And under Section 263(1)(b), any freelancer whose total gross receipts exceed Rs 5 lakh is required to furnish a return. Kabir crossed all three thresholds without realising it.

Mistake 5: Invisible to banks and lenders

A year after skipping his filing, Kabir applied for a home loan. The bank asked for three years of ITRs as proof of income. His application was rejected instantly.

For freelancers and small business owners, the ITR is not just a tax document — it is the primary evidence of financial existence in the formal credit system. Without it, you cannot get a home loan, a business loan, a car loan, or a visa to most countries. For freelancers and consultants, ITR filing requires reconciling income from multiple clients with TDS deducted, claiming professional expenses accurately, paying advance tax if estimated liability exceeds Rs 10,000, and choosing the correct ITR form — typically ITR-3 or ITR-4. It is an annual process that takes a few hours. Missing it costs far more.

Bonus: The tool that could have cut Kabir's tax bill in half — Section 58

Had Kabir known about Section 58 of the Income-Tax Act, 2025 — the Presumptive Taxation provision — his situation would have looked very different. This is the correct, updated equivalent of the old Section 44ADA under the 1961 Act.

Under Section 58(2), Table, Sl. No. 3, if you carry on a specified profession as referred to in Section 62(4) of the Act (which covers professions including legal, medical, engineering, architectural, accountancy, technical consultancy, interior decoration, and other notified professions), you qualify as a "Specified Assessee." The manner of computation is clear and generous: 50% of gross receipts, or the profit claimed to have been actually earned, whichever is higher, is your taxable income — and you need not justify or prove any expenses beyond this.

The turnover limits under Section 58 for this category are:

- Up to Rs 50 lakh — standard limit

- Up to Rs 75 lakh — if the amount or aggregate of amounts received in cash does not exceed 5% of total gross receipts (i.e., 95%+ receipts are through banking/digital channels)

For Kabir, earning Rs 10 lakh entirely through bank transfers from clients, Section 58 would have applied. His taxable income would have been just Rs 5 lakh (50% of Rs 10 lakh) — well within the zero-tax rebate threshold under the new regime (Section 156(2)), potentially making his entire tax liability nil.

Two important safeguards in Section 58 to be aware of:

Under Sub-section (3), if you declare profit lower than the Section 58(2) computed figure AND your total income exceeds the maximum non-chargeable amount, you must maintain full books of account under Section 62 and get a tax audit under Section 63.

Under Sub-section (7), if you declare profits lower than required under Sub-section (2) for any year, and your income exceeds the exemption limit, you become ineligible for the presumptive scheme for the five tax years following that year. So once you opt in, declare honestly.

Advance tax for Section 58 users — a special benefit

Taxpayers using the presumptive scheme can skip all quarterly advance tax payments and pay 100% of their advance tax in a single instalment by 15 March. For Kabir, this would have simplified his entire year — one payment in March, one ITR filing in August, and zero notices.

The complete picture: what Kabir's year actually cost him

| Item | Amount |

| Late filing fee (Section 428) | Rs 5,000 |

| Interest on unpaid tax (Section 423) | Rs 6,000+ |

| Frozen TDS refund (Section 431) | Rs 60,000 locked |

| Home loan application | Rejected |

| Total avoidable damage | Rs 71,000+ and counting |

All from skipping a filing that would have taken a few hours — and could have been made far simpler using Section 58.

The bottom line

TDS deducted by your clients is not the end of your tax story — it is the beginning. The ITR is where you reconcile, claim refunds, report foreign assets, carry forward losses, and maintain your financial credibility. For freelancers and small business owners under the Income-Tax Act, 2025, it is not optional — it is foundational.

If you are a professional with gross receipts under Rs 75 lakh and 95%+ digital receipts, Section 58 is your biggest friend. It halves your taxable income automatically, keeps your compliance simple, and — combined with the Section 156(2) rebate — can bring your tax liability to zero.

Kabir's story does not have to be yours. Need help filing correctly under the Income-Tax Act, 2025? Reach out to Virtualca Services — we'll make sure you never receive that notice.

Comments