Section 87A Rebate — The Complete Guide to Making Your Income Tax Zero Legally

Budget 2025 made a headline promise: no income tax up to Rs 12 lakh. That promise is delivered through a single provision — the rebate under Section 87A of the old Act, now re-enacted as Section 156 of the Income-Tax Act, 2025. For millions of salaried employees, self-employed professionals, and small business owners, this rebate is the difference between paying tens of thousands in tax and paying nothing at all.

But it comes with rules, exclusions, and at least one major trap that has caught equity investors completely off guard. Here's everything you need to know.

What exactly is the rebate and how does it work?

The rebate is not a deduction that reduces your income. It is a direct reduction of your computed tax liability. The sequence matters: first the tax is calculated on your income using the slab rates under Section 202(1), and then the rebate is applied to wipe it out entirely — if you qualify.

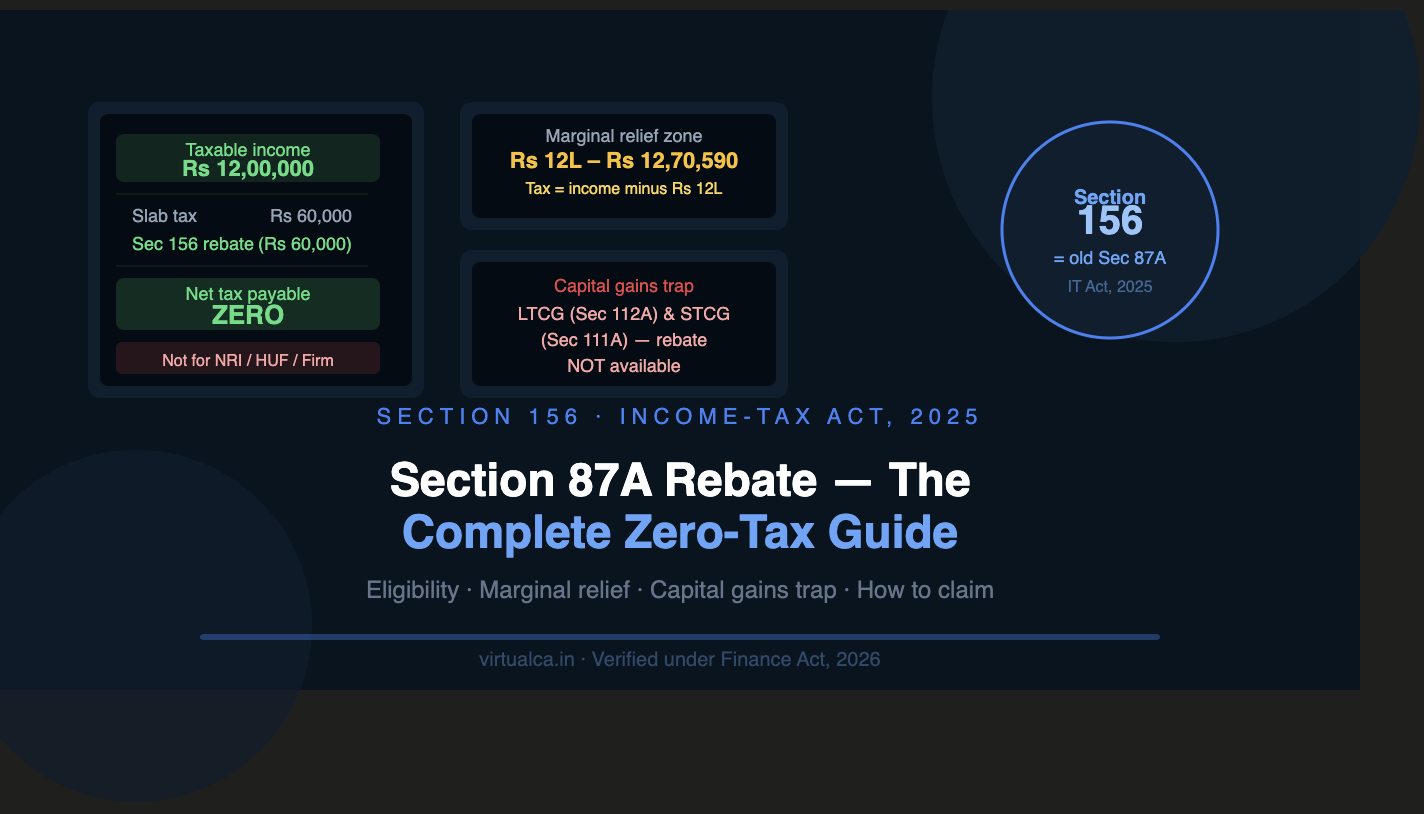

Under Section 156(2)(a) of the Income-Tax Act, 2025, if your total taxable income does not exceed Rs 12,00,000, you receive a rebate equal to 100% of your income tax liability or Rs 60,000, whichever is lower. Since the slab tax on exactly Rs 12 lakh works out to precisely Rs 60,000, both figures match — and your net tax becomes zero.

For salaried employees, the practical threshold is higher. The Rs 75,000 standard deduction under Section 19(1) means your gross salary can be up to Rs 12,75,000 — and after the standard deduction, your taxable income drops to exactly Rs 12,00,000. Under the new tax regime, the threshold is significantly higher at Rs 12 lakh, and a salaried taxpayer with gross income up to Rs 12.75 lakh effectively pays zero tax.

Who qualifies — and who doesn't

The rebate is not available to everyone. Three exclusions catch people by surprise:

NRIs (Non-Resident Indians) are not eligible — they pay tax at slab rates from the first rupee, subject to DTAA provisions. HUFs (Hindu Undivided Families) are also ineligible — the rebate is available only to individual taxpayers, not HUFs, firms, or companies.

So if you are a resident individual filing your own ITR under the new tax regime, you qualify. If you're an NRI, a HUF, a partnership firm, or a company, the rebate simply does not apply to you.

The old regime rebate of Rs 12,500 for income up to Rs 5 lakh continues under Section 156(1) for those who remain on the old regime — but given the dramatically higher threshold under the new regime, the old-regime rebate is only relevant for a narrow group of taxpayers who choose the old regime specifically for its deduction benefits.

Marginal relief: the safety net above Rs 12 lakh

One of the most common fears around this rebate is the "tax cliff" — the anxiety that earning Rs 1 above Rs 12 lakh would suddenly trigger a Rs 60,000 tax bill. Section 156(2)(b) prevents this through marginal relief.

The formula is elegant: if your income exceeds Rs 12 lakh and the tax you'd otherwise owe exceeds the amount by which your income exceeds Rs 12 lakh, your tax is capped at that excess. In plain numbers: if your taxable income is Rs 12,05,000, your slab tax without relief would be Rs 60,750. But under marginal relief, your tax is capped at Rs 5,000 — the amount by which your income exceeds Rs 12 lakh.

According to ITR Validation Rule 191, this relief applies until your taxable income (excluding certain capital gains) reaches Rs 12,70,590. Beyond that point, the normal slab-rate tax is lower than the marginal relief cap, and standard rates apply. The rebate and relief together create a smooth, continuous transition rather than a painful cliff.

Step-by-step: how to claim the rebate

The good news is that you don't need to manually calculate or claim this rebate in a separate form. The ITR filing portal applies it automatically when your total income meets the criteria. But understanding the inputs ensures you don't accidentally disqualify yourself:

Start with your gross salary and all income from every source — salary, bank interest, rental income, capital gains, everything. Apply the Rs 75,000 standard deduction if you are salaried (Section 19). Apply any permitted deductions under the new regime such as employer NPS contributions under Section 124(2). Arrive at your total taxable income. If that figure is Rs 12,00,000 or less, the portal computes the slab tax and then zeroes it out through the rebate.

The key error to avoid: forgetting to include bank interest, FD interest, or other income from other sources. Many taxpayers mentally calculate their "salary minus standard deduction" and assume that's the total income. It isn't — every rupee of income from every head counts toward the Rs 12 lakh threshold.

The capital gains trap — officially clarified by the IT Department

This is the part that has genuinely surprised thousands of equity investors and mutual fund holders. If you have long-term capital gains from listed equity shares or equity mutual funds (taxed under Section 112A at 12.5%) or short-term capital gains from equity (taxed under Section 111A at 20%), the rebate does not apply to the tax on those gains.

The Income Tax Department has officially clarified that the Rs 60,000 rebate under the new tax regime is not available on incomes taxed at special rates, including capital gains from equity and lotteries. It is available only on the tax payable as per the normal slab rates under Section 202(1) of the Income-Tax Act, 2025.

Here's what this means practically. Suppose your salary income after the standard deduction is Rs 8 lakh, and you also have Rs 2 lakh in short-term capital gains from equity shares. Your total income is Rs 10 lakh — well within the Rs 12 lakh rebate threshold. Your slab-rate tax on Rs 8 lakh of salary income is Rs 20,000, which the rebate wipes out. But the Rs 2 lakh STCG is taxed separately at 20% — that's Rs 40,000 in tax that the rebate cannot touch.

Even if an individual's total income qualifies for the rebate, if any part of that income includes long-term capital gains under Section 112A from the sale of equity shares or equity mutual funds, the rebate is not available on that portion. This applies equally to STCG under Section 111A. The rebate zeroes out your slab-rate tax, but special-rate income remains taxed at its prescribed rate regardless of your total income level.

For investors who hold equity mutual funds or stocks and also have salary income near the Rs 12 lakh boundary, this is a critical planning point. Realising large gains in a year where your income is near the threshold can result in an unexpected tax bill even when you expected to pay nothing.

Other disqualifying situations to watch for

Filing late does not eliminate the rebate itself, but it attracts a fee under Section 428 — Rs 5,000 if your income exceeds Rs 5 lakh, Rs 1,000 otherwise. Filing on time preserves your full benefit.

Getting your residency status wrong is a more serious error. If you spent sufficient time outside India in a tax year to be classified as a non-resident, you lose the rebate for that entire year — even if you spent most of the year in India.

Online gaming and lottery winnings are taxed at special rates and are similarly excluded from the rebate, just like Section 112A gains.

The bottom line

Section 156 of the Income-Tax Act, 2025 — the legal successor to the beloved Section 87A — is genuinely one of the most generous income tax provisions in Indian tax history. Zero tax on income up to Rs 12 lakh, with a smooth marginal relief corridor extending to Rs 12,70,590, and automatic application through the ITR portal.

The catch is in the details: you must be a resident individual, your total income from all sources must stay within the limit, and if you have equity capital gains, those remain taxable regardless of your other income.

Plan carefully, include every income source in your calculation, and if you're an investor, time your capital gains with awareness of how they interact with the rebate.

Have questions about whether you qualify for zero tax this year? Reach out to Virtualca Services — we'll check your numbers.

Comments