Marginal Relief Explained — Why Earning Rs 12.01 Lakh Doesn't Mean Paying Rs 60,000 in Tax

Here's a question that makes a lot of taxpayers anxious: if income up to Rs 12 lakh is completely tax-free under the new regime, what happens the moment you earn one rupee more?

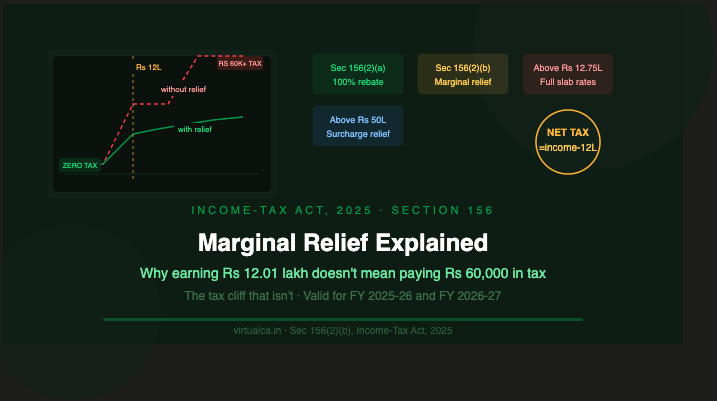

Without knowing the answer, it looks terrifying. Your tax jumps from zero to over Rs 60,000 for a single extra rupee of income. But that "tax cliff" is largely a myth — and the provision that prevents it is called Marginal Relief.

First, why does the cliff exist at all?

Under Section 202(1) of the Income-Tax Act, 2025, the new tax regime applies these slabs:

- Up to Rs 4,00,000: Nil

- Rs 4,00,001 to Rs 8,00,000: 5% — tax of Rs 20,000

- Rs 8,00,001 to Rs 12,00,000: 10% — tax of Rs 40,000

- Rs 12,00,001 to Rs 16,00,000: 15%

At exactly Rs 12 lakh, your gross slab tax is Rs 60,000. But Section 156(2)(a) provides a 100% rebate — wiping out that entire Rs 60,000 — so your net tax is zero.

The problem: cross Rs 12 lakh by even Rs 1,000, and the full rebate under clause (a) disappears. Your slab tax on Rs 12,01,000 is Rs 60,150. Without any safety net, you would owe Rs 60,150 for earning Rs 1,000 more than the threshold. You'd be Rs 59,150 poorer for a small pay rise. This is the sudden tax jump that marginal relief is specifically designed to prevent.

The rescue: Section 156(2)(b)

Section 156(2)(b) of the Income-Tax Act, 2025 is the marginal relief provision. In plain English, it says: if your income exceeds Rs 12 lakh and the tax you'd otherwise owe is more than the amount by which your income exceeds Rs 12 lakh, then your tax is capped at exactly that excess.

The formula is simple:

Net tax payable = Total income − Rs 12,00,000

So for Rs 12,01,000 income, your tax is capped at Rs 1,000 — not Rs 60,150. For Rs 12,10,000 income, your tax is capped at Rs 10,000. The government ensures you never pay more in tax than the extra income you actually earned.

Marginal relief ensures that the additional tax payable is not more than the income exceeding Rs 12 lakh, preventing a sudden increase in tax liability when income crosses the rebate threshold.

The comparison table: relief in action

This is where the numbers become impossible to ignore. All figures exclude Health & Education Cess for simplicity.

| Total taxable income | Tax as per slabs (Sec 202) | Marginal relief (Sec 156) | Net tax payable |

| Rs 12,00,000 | Rs 60,000 | Rs 60,000 (full rebate) | NIL |

| Rs 12,01,000 | Rs 60,150 | Rs 59,150 | Rs 1,000 |

| Rs 12,10,000 | Rs 61,500 | Rs 51,500 | Rs 10,000 |

| Rs 12,50,000 | Rs 67,500 | Rs 17,500 | Rs 50,000 |

| Rs 12,70,590 | Rs 70,589 | Rs 1 | Rs 70,588 |

| Rs 12,80,000 | Rs 72,000 | NIL | Rs 72,000 |

The pattern is clear: in every case between Rs 12 lakh and the cutoff point, your net tax equals exactly what you earned above Rs 12 lakh. Not a rupee more. The relief shrinks gradually as your income rises, instead of hitting you with a sudden cliff.

Where does marginal relief stop?

Marginal relief is available for taxable incomes up to approximately Rs 12.75 lakh. Beyond this point, the normal slab tax becomes lower than the "excess income" calculation, and the relief naturally fades out.

The precise threshold validated under ITR Rule 191 for AY 2026-27 is Rs 12,70,590. At this income level, the slab-based tax and the marginal relief formula converge. Beyond Rs 12,70,590, the standard slab rates are more beneficial than the relief cap, and you simply pay the normal slab tax.

One important practical note confirmed by Tax Garden: the Income Tax Bill 2025, which takes effect from FY 2026-27 (AY 2027-28), renumbers Section 87A as Section 156, with the substantive provisions remaining the same. So whether you encounter references to Section 87A (under the 1961 Act) or Section 156(2)(b) (under the 2025 Act), they describe the same protection.

Salaried employees: the Rs 12.75 lakh sweet spot

For salaried individuals, there is an additional layer of protection. Under Section 19(1) of the Income-Tax Act, 2025, a standard deduction of Rs 75,000 is available under the new regime. This means a salaried employee with a gross salary of Rs 12,75,000 has a taxable income of exactly Rs 12,00,000 — fully within the zero-tax rebate zone.

Salaried taxpayers earning up to Rs 12.75 lakh pay no tax due to the Rs 75,000 standard deduction combined with the Rs 60,000 rebate under the new regime. For salaried employees, the effective cliff is not at Rs 12 lakh of taxable income — it begins at Rs 12.75 lakh of gross salary.

Bonus: marginal relief also exists for high earners — surcharge thresholds

Marginal relief is not just a tool for the Rs 12–13 lakh income band. It operates identically at the surcharge thresholds for high-income taxpayers.

Marginal relief can be claimed from surcharge if income earned exceeds Rs 50 lakh, Rs 1 crore, Rs 2 crore, or Rs 5 crore under the old regime, and Rs 50 lakh, Rs 1 crore, or Rs 2 crore under the new regime. In each case, the principle is the same: the extra tax triggered by crossing a threshold cannot exceed the extra income that caused the crossing. A business owner earning Rs 50,01,000 is protected from a sudden surcharge spike just as effectively as a salaried employee earning Rs 12,01,000 is protected from a rebate cliff.

What marginal relief does NOT cover

There are two important exclusions worth noting. First, marginal relief under Section 156 applies only to resident individuals — Non-Resident Indians are not eligible. Second, the rebate and relief cannot be applied against tax on long-term capital gains under Section 112A (equity shares and equity mutual funds). If your total income crosses Rs 12 lakh because of LTCG on listed equity, the relief may not fully apply to that component. This is a detail that trips up investors and is worth verifying with a tax professional.

The bottom line

The tax cliff at Rs 12 lakh is real on paper, but marginal relief under Section 156(2)(b) of the Income-Tax Act, 2025 ensures it almost never hurts you in practice. In the danger zone between Rs 12 lakh and Rs 12,70,590, your tax equals exactly the amount by which your income exceeds Rs 12 lakh — no more. Above Rs 12,70,590, normal slab rates apply, and they are entirely predictable.

Understanding this mechanism removes one of the most common anxieties in Indian tax planning: the fear that a small raise or a modest freelance payment can suddenly trigger a five-figure tax bill. It can't — and now you know exactly why.

Need help calculating your precise tax position for FY 2025-26? Reach out to Virtualca Services — we'll map out your numbers to the rupee.

Comments