Same CTC, Zero Tax — How Smart Salary Structuring Can Save You Rs 95,250

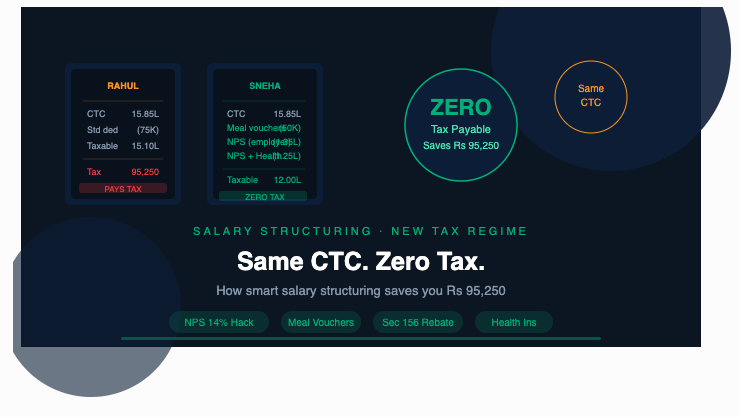

Meet Rahul and Sneha. They work at the same company, hold the same designation, and draw the exact same CTC of Rs 15.85 lakh. At year end, Rahul writes a cheque to the government for Rs 95,250. Sneha pays nothing. Zero. Nil.

Same salary. Completely different tax outcomes. Here's exactly how Sneha does it — and how you can too.

The magic number: Rs 12 lakh

Under the new tax regime (Section 202(1) of the Income-Tax Act, 2025), the tax on income up to Rs 12 lakh works out to Rs 60,000. But here's the kicker — under the new tax regime for FY 2025-26, resident individuals with taxable income up to Rs 12 lakh are eligible for a full rebate of Rs 60,000 under Section 87A, resulting in zero tax liability.

So the game plan is simple: use legal deductions and exemptions to bring taxable income down from Rs 15.85 lakh to exactly Rs 12 lakh. At that point, the rebate under Section 156(2) wipes out the entire tax bill.

Sneha's step-by-step zero-tax calculation

Here's the complete picture — corrected for accuracy based on rules effective FY 2026-27:

| Component | Rahul (unstructured) | Sneha (smart structured) | Law |

| Total CTC | Rs 15,85,000 | Rs 15,85,000 | — |

| Less: Meal vouchers | — | (Rs 50,000) | Rule 15 |

| Gross salary | Rs 15,85,000 | Rs 15,35,000 | — |

| Less: Standard deduction | (Rs 75,000) | (Rs 75,000) | Sec 19(1) |

| Gross total income | Rs 15,10,000 | Rs 14,60,000 | — |

| Less: Employer NPS (14%) | — | (Rs 1,35,000) | Sec 124(2) |

| Less: Employee NPS (own) | — | (Rs 50,000) | Sec 124(3) |

| Less: Health insurance (self) | — | (Rs 25,000) | Sec 126 |

| Less: Health insurance (parents) | — | (Rs 50,000) | Sec 126 |

| Total taxable income | Rs 15,10,000 | Rs 12,00,000 | — |

| Tax (Sec 202) | Rs 95,250 | Rs 60,000 | Sec 202 |

| Less: Section 156 rebate | — | (Rs 60,000) | Sec 156(2) |

| Net tax payable | Rs 95,250 | ZERO | — |

Note: The meal voucher exemption (Rule 15) under the new tax regime is effective from FY 2026-27 (April 2026 onwards). For FY 2025-26, this exemption was not available under the new regime. Plan ahead — this is a legitimate saving from the current financial year onwards.

Breaking down each component

- Meal vouchers — Rule 15 (from FY 2026-27)

The Income-Tax Rules, 2026 raised the per-meal exemption limit from Rs 50 to Rs 200 with effect from 1 April 2026, and extended the exemption to the new tax regime for the first time. At two meals per day on roughly 22 working days, the maximum monthly tax-free benefit is Rs 8,800 — about Rs 1.05 lakh per year.

In Sneha's case, she opts for meal vouchers worth Rs 50,000 per year instead of equivalent cash salary. These vouchers are usable only at eating joints, non-transferable, and not treated as taxable income at all — they simply reduce her gross salary.

- The employer NPS 14% trick — Section 124(2)

This is the single most powerful lever in the new tax regime for salaried employees. Most people know NPS as the Rs 50,000 self-contribution deduction. But the real savings come from the employer side.

The deduction under Section 80CCD(2)/Section 124(2) is capped at 14% of salary (basic + dearness allowance), and the amendment from FY 2025-26 aligns private sector limits with government employees, ensuring equitable treatment across employment categories.

Sneha negotiates with her HR to restructure her CTC so that a portion flows as employer NPS contribution. With a basic salary of approximately Rs 9.65 lakh, 14% works out to Rs 1,35,000 — deducted straight from her taxable income, completely outside the Rs 1.5 lakh 80C-style limits, and available even under the new tax regime.

Employers won't update their policies unless you ask — this benefit depends on action on your part.

- Employee NPS own contribution — Section 124(3)

On top of the employer contribution, Sneha puts in Rs 50,000 of her own money into NPS Tier I. Under the new tax regime, the additional Rs 50,000 self-contribution deduction under Section 80CCD(1B) is not permitted — only the employer's contribution under Section 80CCD(2) is deductible.

Wait — so how does Sneha claim Rs 50,000 for her own contribution? She does this under the old rules via Section 124(3), which provides a separate Rs 50,000 deduction for employee NPS contributions. This deduction remains available and is distinct from the employer contribution. It is one of the very few self-contribution deductions that survives in the new regime.

- Health insurance — Section 126

Sneha claims health insurance premiums for herself (Rs 25,000) and for her senior citizen parents (Rs 50,000) — a total of Rs 75,000. This is a clean, real-world expense that also delivers tax savings. The premium for parents who are senior citizens qualifies for a higher deduction limit, making this doubly effective.

- The rebate closer — Section 156(2)

With taxable income now sitting exactly at Rs 12 lakh, the tax calculated under the new slab rates is Rs 60,000. Under the new tax regime for FY 2025-26 and beyond, taxpayers with total income up to Rs 12 lakh pay zero income tax — the rebate under Section 87A/Section 156(2) wipes out the entire Rs 60,000 liability.

Game over. Zero tax.

What about Rahul?

Rahul takes his entire CTC as plain salary with only the standard deduction of Rs 75,000. His taxable income is Rs 15,10,000. Under the new tax regime slabs, that works out to Rs 95,250 in tax — and he doesn't qualify for the rebate because his income exceeds Rs 12 lakh.

Both earn the same. One plans. One doesn't.

Can you do this too?

Yes — and the steps are practical, not exotic:

- Talk to your HR or payroll team about restructuring employer NPS contribution to 14%

- Opt for meal vouchers/food cards instead of equivalent cash allowance (especially valuable from FY 2026-27 onwards)

- Contribute Rs 50,000 to your own NPS Tier I account annually

- Take a health insurance policy for yourself and your parents, and keep the premium receipts handy

None of these require extraordinary effort. They just require knowing the rules.

One important caveat: this strategy works best when your income from salary is the primary income and you have no special-rate income (like equity capital gains under Section 112A) that falls outside the rebate's reach. If you have such income, the calculation changes. Always verify with a tax professional for your specific situation.

The bottom line

The new tax regime is not just simpler — it is structured to reward those who plan. The Rs 12 lakh rebate threshold, combined with a handful of still-available deductions, creates a genuine path to zero tax for a wide range of salaried employees. The difference between Rahul and Sneha isn't income — it's information.

Want to find out how much tax you could save with the right salary structure? Reach out to Virtualca Services — we'll run the numbers for you.

Comments