PF Withdrawal When Switching Jobs — The Tax Traps Nobody Warns You About

You've just accepted a great new offer. The excitement is real. And then someone at work says: "Hey, don't forget to withdraw your PF before you leave — it's your money after all."

Stop right there. That well-meaning advice could cost you a significant chunk of your own savings in taxes and penalties. Here's everything you actually need to know about your Provident Fund when you switch jobs — backed by the Income-Tax Act, 2025 and the latest EPFO rules.

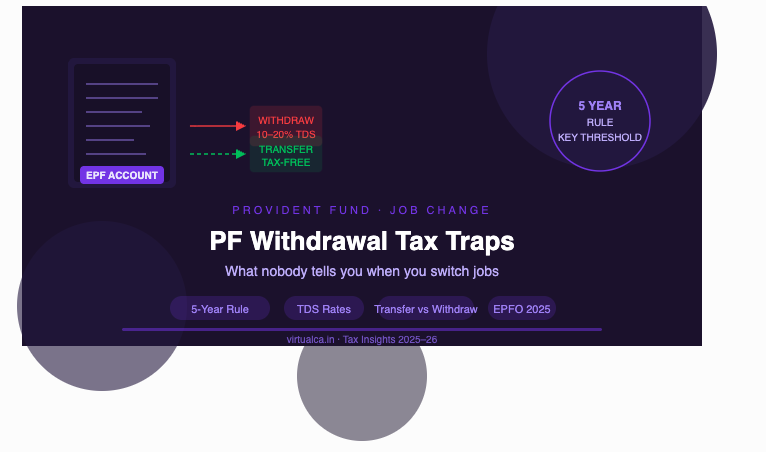

The one number that changes everything: 5 years

Under Schedule XI, Part A, Paragraph 8 of the Income-Tax Act, 2025, your entire accumulated EPF balance — employee contributions, employer contributions, and all the interest earned — is fully exempt from tax, but only if you have completed five years of continuous service.

EPF contributions are eligible for deduction under Section 80C, and interest and maturity amounts are tax-free only if the employee completes five years of continuous service.

The good news? Switching jobs does not automatically reset this five-year clock — provided you transfer your PF rather than withdraw it. The law explicitly says that if you move your balance from a previous employer's Recognised Provident Fund (RPF) to a new one, your service period with the previous employer counts toward the five-year total.

What happens if you withdraw before five years

If you choose to withdraw before hitting the five-year mark — and none of the exemptions apply — the withdrawal becomes fully taxable. And TDS kicks in immediately.

Under Section 392(7) of the Income-Tax Act, 2025:

- TDS is applicable when the EPF withdrawal exceeds ₹50,000 and the employee has not completed five years of continuous service. With a valid PAN, TDS is deducted at 10%.

- Without a valid PAN — or if your PAN is not linked to Aadhaar — the TDS rate jumps to 20% under Section 397. That means one in five rupees of your own savings goes straight to the government before you even see it.

Important: TDS is not your final tax liability. It is advance tax. When you file your ITR, the withdrawal amount gets added to your total income for the year and taxed at your applicable slab rate. If you are in the 30% bracket, the effective tax hit on an early PF withdrawal can be substantial.

PAN–Aadhaar linking: non-negotiable

With the implementation of the New Labour Codes and recent Union Budget updates, the "tax-free" status of your PF now comes with fine print — including the ₹7.5 lakh combined employer contribution cap and strict conditions around the five-year service rule.

Under the validation rules for AY 2026-27, your PAN must be linked with Aadhaar. If it is not, you are treated as someone who has not furnished a PAN at all — which triggers the higher 20% TDS rate. Check your linking status on the Income Tax e-filing portal before initiating any PF claim.

When early withdrawal is still tax-free

The law is fair enough to recognise that not every job exit is a choice. Under Schedule XI, Part A, Paragraph 8(1)(b), you can withdraw your PF before five years without any tax liability in three situations:

- Your service ended due to your own ill-health

- The employer's business was contracted or shut down

- The termination happened due to any cause beyond your control — such as redundancy or company-wide layoffs

In these cases, the full accumulated balance remains tax-exempt regardless of how many years you have served.

Transfer: always the smarter move

Every financial advisor, tax expert, and the law itself points in the same direction — transfer, don't withdraw.

EPF transfers now happen automatically when you join a new employer and the new employer updates your date of joining, since your Universal Account Number (UAN) remains the same throughout your career. You no longer need to file a manual Form 13 in most cases. Transfers that once took 30 to 45 days are now being completed in 7 to 10 days, thanks to Aadhaar-based e-Sign and API integration with employer HR systems.

Why is transferring so much better?

- Your five-year service clock keeps running uninterrupted

- The balance continues compounding at the EPF interest rate confirmed by the EPFO Central Board of Trustees for year on year

- Your future withdrawal (after the five-year mark) will be completely tax-free

- Your EPS pension eligibility is preserved — withdrawing resets this entirely

The bottom line

Your EPF is not a bonus to cash out when you change jobs. It is a tax-sheltered retirement corpus that grows at EPO Interest rate, fully tax-free — but only if you play by the rules. Withdrawing early hands over a chunk of your savings to the taxman without any real need to.

Transfer your PF, keep your UAN active, and ensure your PAN is linked to Aadhaar. Those three steps cost you nothing and protect everything.

Not sure how to handle your PF during a job transition? Reach out to us at Virtualca Services — we'll help you make the right move.

Comments